Public finance: A budget and financial statement system shall be instituted. The spheres of financial administration of central and local governments shall be defined. Economizing and frugality shall be enforced. The budget shall be steadily balanced and capital accumulated for the country's production.

The tax policy of the state shall be based on the principle of ensuring supplies for the revolutionary war and taking into account the rehabilitation and development of production and the requirements of national construction. The tax system shall be simplified and equitable distribution of burden effected.

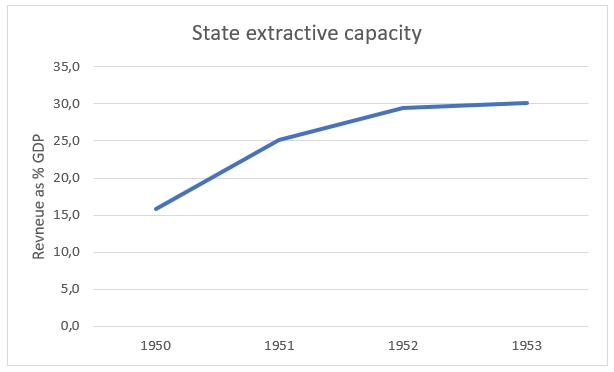

During the Qing period, imperial government revenues never exceeded 4% of the country’s gross domestic product (GDP). The imperial taxation system, primarily based on agricultural production, generally featured low tax rates compared to Western Europe. However, the system faced challenges in efficient revenue collection and may not have been optimally designed to fund investments in infrastructure and development. After 1911,the national fiscal system had collapsed, and foreign and domestic loans had to fill the gap. The GMD government was only able to extract 8,8% of GDP in 1936. It was the best year for GMD administration.

The government of the PRC reached in 1950 16% and in 1953 more than 30% of GDP.

Fig. 40.1 Extraction 1950-1953

Source: Wang (2011). Page 231

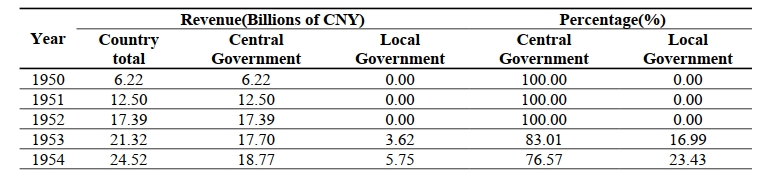

In general, the financial management system comprises the budget, taxation, enterprise financial, and capital construction management systems. The management principles of the PRC include unified leadership, hierarchical management, and financial classification. Hierarchical management delineates local fiscal revenue, establishes a local-level budget, and formulates region-specific implementation methods. Financial classification organizes national finance into central government, province (municipality), and county levels, with county finances managed at the county and community levels. Financial management encompasses revenue and expenditure budget management, with indicators issued annually and income required to increase.

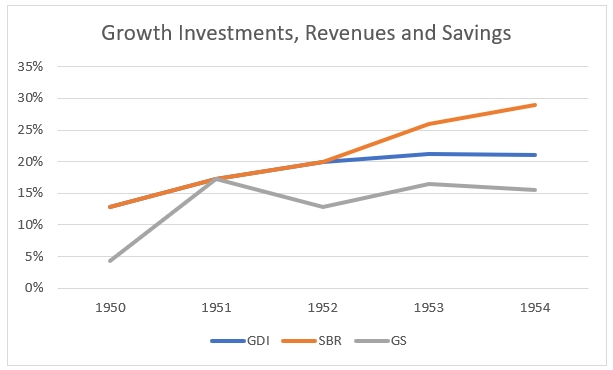

Fig. 40.2 State Budget 1950-1954

Figure 40.1b shows the increase of gross domestic investment in material things from 13% in 1950 to 21% in 1954 of GNP. One result of this effort was that industrial

production rose during the decade at an average annual rate of 20%. The state budget revenues rose very rapidly from 12,7% in 1950 to 29% in 1954. Government saving (revenues less government consumption) also kept pace; such saving financed a growing proportion of total investment. The main source of state revenue gains was the profits and depreciation allowances of state enterprises (average of 36%).

"This increase was owing to the extension of state control over industrial enterprises, relatively high prices on industrial products and low wages, and the growth of depreciation allowances based on enlargement of the capital stock. State enterprises turned over almost all of their gross profits to the state, except for the retention of small bonus funds.."

The agriculture taxes declined from 33% in 1950 to 12% in 1954.

Increase production

Ultimately, a government's capacity to obtain resources depends on its ability to ensure taxpayer cooperation. A wide-ranging compliance base guarantees sufficient revenue for the state. Conversely, if tax evasion becomes widespread or evolves into a common practice, the government is likely to encounter financial difficulties. In such circumstances, meeting fiscal commitments may pose significant challenges for the government. Without the Communists' success in expanding revenue streams, the newly established PRC would have struggled to manage inflation, solidify its authority, cover the expenses of the Korean War, revive the economy to prewar levels, and lay the groundwork for the imminent socialist transformation. The CCP had two decades of experience in taxing the peasantry by 1949, developing various methods applicable to diverse socioeconomic conditions across China. Initial experiments with a proportional 15% tax on agricultural income evolved into a more nuanced graduated tax system, notably used during the Anti-Japanese War. Unable to implement radical wealth redistribution during the second United Front, the CCP employed a progressive tax schedule to maintain peasant support and build confidence. Recognizing the potential of tax policies beyond revenue collection, the CCP introduced incentives for increased production and used tax laws for propaganda and education, fostering patriotism and class consciousness. After the expulsion of the Japanese, the CCP adapted to new priorities, shifting from the previously established tax systems under the United Front. In 1946, as land reform regained prominence, the CCP opted for a proportional tax system, introducing a standard deduction per taxpaying household. This approach retained the progressive tax element, where the wealthy paid higher taxes, but it also shifted the burden towards middle-income households. Implemented from 1946 to 1949, this proportional tax system was administered by the Party and the PLA in post-land reform areas.

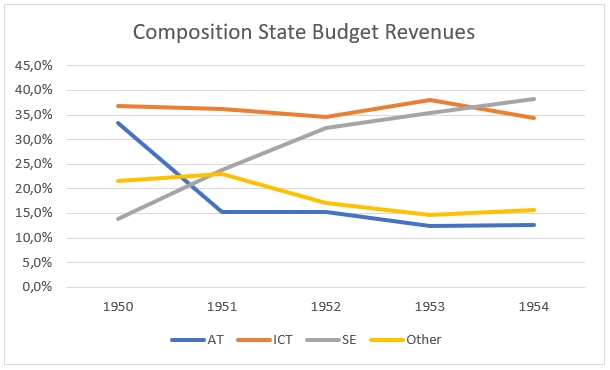

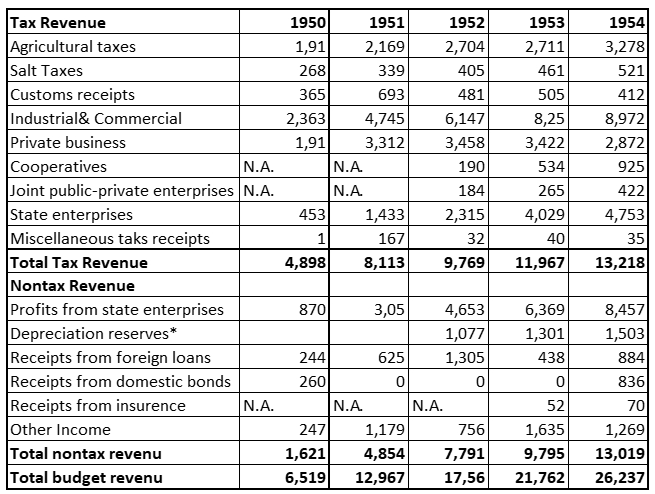

Fig. 40.3 Taxes 1950-1954

Source: Macrae (1969). Page 84

Figure 40.3 shows how the tax revenues of the agricultural sector stabilized around the 1952 level. Figure 40.6 shows more details.

Due to the CCP's lack of experience with urban taxation, the old tax system in cities was initially retained. The swift takeover of Shanghai by the PLA allowed little time to devise new policies, so initially, the new government opted to preserve the GMD system of tax collection temporarily. To generate revenue from businesses as a last resort, a policy of "self-reporting and full payment; light taxes but severe punishments" was implemented. This approach essentially refined the previous business tax system by offering incentives and penalties, but it was deemed suitable given the limited resources available. Collections increased from June to August of 1949, enabling Shanghai to meet its financial obligations.

Public finance...

The development of accounting in China unfolded within a vast nation with an underdeveloped profession. In the initial phases after the establishment of the People’s Republic, the field faced delays and shortages in knowledge and human capital, prompting an initial surge in demand for accounting expertise and professionals.

Late 1949, China adopted a comprehensive economic accounting system, influenced by Soviet theory and experience. Initially implemented in industrial enterprises under the Northeast People's Government's Ministry of Industry, directives were issued to conduct physical asset inventories, establish statistical reporting, financial and cost accounting, budgetary control, production and cost standards, and clarify responsibilities within the organizational structure. The system emphasized mass participation, economic practices, production emulation campaigns, incentives, and worker involvement in management.

On the national level, the GAC called for economic accounting in 1951, following earlier regulations on economic policy and administration. Starting from 1950, efforts were made to standardize accounting systems in state enterprises, with regulations covering budget preparation, review, and a census of industrial and mining enterprises in mid-1950. The government also provided guidance to private companies and small businesses on implementing accounting and invoice systems.

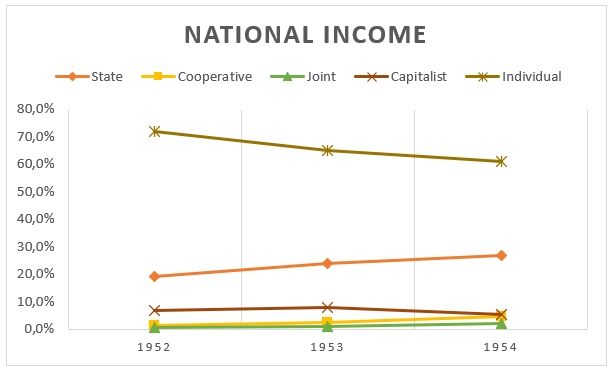

Fig. 40.4 National income by ownership of enterprise 1952-1954

Source: Chen (2017). Page 143 At 1952 prices

On March 3, 1950, the GAC passed a decision on the unification of national financial and economic work. It highlights the necessity of coordinating national financial and economic efforts to address fiscal imbalances and potential inflationary risks. The document outlines specific measures, including the establishment of committees, austerity measures, centralized management of public grain, unified allocation of taxes, and to establish uniform accounting systems. It emphasizes strict enforcement and warns of legal consequences for non-compliance. The document also acknowledges the challenges faced by local leaders in the transition but stresses the importance of active and responsible attitudes in future financial and economic work. The national financial organs had to approve all items of expenditure under the state budget. Local needs were admittedly secondary; national priorities were to come first. On August 19, 1951, this directive was partly reversed, specific taxes were categorized as central income, while other taxes were allocated to both the central and local levels in proportion. Additionally, certain sources of income were designated for either the region or the province. Administrative expenses were distributed, allowing the center and locality to independently manage their disbursement.

The 1951 directive specified five methods for establishing the economic accounting system for industrial enterprises: (1) planned management involving production, labor productivity, and cost reduction targets, along with an "inspection system" to ensure goal attainment, (2) determination of required capital and allocation of excess funds among enterprises with inadequacies, (3) an independent accounting system, centralized credit transactions, and manager responsibility for profit performance, (4) granting enterprises the right to enter contracts for raw materials and product sales, and (5) the institution of a factory bonus fund plan, offering a bonus for overfulfillment of profit plans.

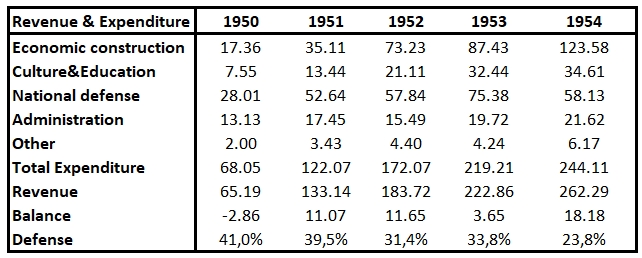

Fig. 40.5 Revenue and Expenditure 1950-1954

China Fiscal Yearbook Data Volume 2006

In October 1949, amidst the ongoing civil war, more than 60% of the total fiscal expenditure of the new government was attributed solely to direct military expenses. Furthermore, the new government had decided to retain former regime military and government personnel who pledged allegiance to the new administration. Additionally, the number of military, government, and administrative personnel in the liberated areas surged from 6 million in August to 7 million in November. This substantial expenditure was primarily funded through the issuance of paper currency. To execute the First Five Year Plan (FFYP) effectively, there was a necessity for a standardized accounting system. However, the accounting practices across business enterprises varied significantly due to differences in ownership structures and administrative methods. This led to a coexistence of traditional Chinese-style bookkeeping and Western accounting systems in use. Consequently, comparing business operations and accounting information across different enterprises or integrating them into state budgets and national economic plans was often impractical. Hence, there was an urgent requirement for the central government to introduce new accounting frameworks to facilitate the socialist transformation of industrial and commercial enterprises on a national scale. Hence, in March 1950, the Central Finance and Economic Commission of the new government provided guidelines for the formulation of standardized industrial accounting systems. Collaborating with Soviet finance and accounting advisors stationed in different government bodies in China, accounting systems inspired by the Soviet model were implemented. The objective was to transform enterprises, which originally operated under diverse ownership structures and administrative frameworks, into a socialist state-owned economy. To facilitate national economic planning and control, a comprehensive inventory of assets and liabilities of all enterprises was deemed essential. By June 1951, thirteen industrial

administration ministries, at the central government, had issued unified accounting systems for the enterprises and economic institutions under their jurisdictions. Only the Soviet style of socialist accounting was allowed for teaching and learning in universities and colleges. Financial and economic educational institutions were established in major administrative districts and departments. The educational framework and curriculum were modelled after Soviet financial and economic colleges. The core courses, encompassing accounting principles, specialized accounting, economic activity analysis, and financial management, were structured in alignment with the Soviet Union's approach. The textbooks primarily originated from two main sources: those employed at Shanghai Lixin Accounting School and translations of Soviet textbooks. All Western textbooks are replaced.

Taxation...

The fiscal system linked to the planned economy, referred to as "unitary remittance and unitary expenditure," was characterized by high centralization and a focus on redistribution. This system limited the autonomy of local governments in both tax collection and spending, providing them with little incentive to foster economic growth.

The initial responsibilities assigned to provincial administrations prioritized tax collection and the sale of bonds to the populace, rather than focusing on land reform. These actions, particularly the compulsory nature of bond sales, led to unrest, including riots, and subsequently resulted in an economic slowdown. During this period, some businesses shut down, and others rejected the new paper currency issued by the government. For a while, the PLA was the most visible arm of the new regime in many areas, providing cover for tax collection efforts.

Until September 1952, products manufactured by state-owned enterprises were exempt from taxes during circulation, and cooperative enterprises enjoyed a one-year tax exemption. In an attempt to avoid wholesale taxes, private businesses began producing directly for retailers. As the state-owned sector didn't contribute taxes and relied on state subsidies, its rapid expansion led to an inevitable inadequacy in the tax revenue collected by the government. The national financial conference in September 1952 decided goods produced by state-owned and private firms would all be taxed equally.

During the initial years of the PRC, the government introduced income tax incentives aimed at encouraging private investment in specific industrial sectors, rather than commerce. The most substantial tax reduction, amounting to 40%, was offered to select machine-building enterprises. Concurrently, state-owned enterprises benefited from preferential exemptions and tax reductions, leading to a redistribution of the tax burden onto private enterprises.

Fig. 40.6 Tax Revenue 1950-1954

The GMD government relied on three forms of tax. The salt tax, land tax and custom duties.

The PRC administration relied on these three forms of tax and was able to tax profits from state enterprises and collect tax from industrial and commercial enterprises.

Wang (2001) takes the situation in Wuhan as an example of the difficulties the new regime faced in collecting taxes. First of all, there were only 532 state enterprises, only 31 joint state-private companies and a few hundred coop enterprises. The private sector was far bigger and existed mostly of small enterprises. Small firms even lacked the basic idea of bookkeeping. The second problem the administration encountered was the tax collection infrastructure. Before 1949, there were 19 tax collection agencies belonging to the national, provincial and municipal administration. In the agencies served 1,622 employees, only one-third remained in office after the take-over by the PLA. The CCP assigned 180 Party cadres and pro-communist students and workers.

The new administration launched several anti-corruption campaigns (i.a. sanfan and wufan see Article 18 and Article 30 ).

"In the minirecession caused by the three-antis and five-antis campaigns, many private enterprises were suffering genuine financial difficulties and hence were not able to pay tax. And the campaigns themselves may have kept businesspeople too busy to keep proper accounts and tax officers too busy to keep track of their accounts, which made it easier to evade taxes." In 1953 nationwide campaign reviewed specifically tax collectors.

In identifying taxpayers, the government made use of several methods: the existing guild structure made identifying taxpayers easy. However, this method had its weaknesses, so, neighbourhood organisations replaced the guilds after 1952."In areas such as Manchuria where land reform had already been completed, grain taxes went up to support a national mobilization effort. Until the end of the war in 1953, grain taxes in Manchuria were as high as fifteen-twenty percent of total crop yield depending on the area and local conditions.208"

Tax paying

Agriculture taxation...

Certain direct taxes were imposed on the agricultural sector, but the impact of "forced saving" (bonds) or taxation on rural areas was predominantly experienced indirectly through low procurement prices for agricultural goods. Peasants had to supply their produce to the state at prices lower than those that would have existed under free market conditions, representing an unequal exchange termed the "scissors gap".

Fig. 40.7 Agriculture Tax Schedule 1950

Source: Shue (1980). Page 106

Agricultural tax collection typically occurred in two seasons, summer and autumn. In regions where summer crops held less significance, the entire tax could be collected in autumn. Payment of the tax was usually made in grain, but under certain circumstances, other agricultural produce or cash could be accepted. Taxpayers were responsible for delivering the taxed commodities to specified centers and covering the transportation costs up to a distance typically equivalent to a day's round trip. Any expenses beyond that distance were to be reimbursed to them.

During the Korean War, the Chinese government implemented policies to support the war effort, which included increasing taxes and encouraging donations from citizens, including farmers.This led to a significant increase in the financial burdens on farmers during that period.

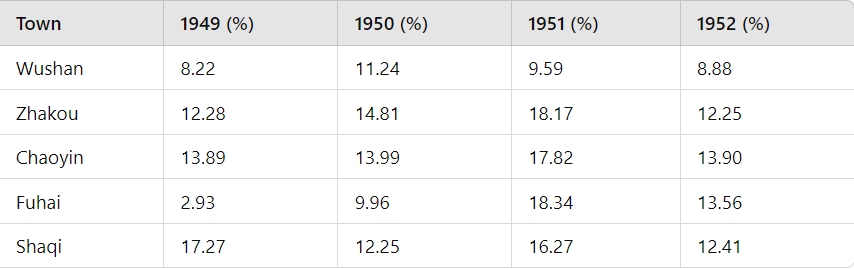

Fig. 40.8 The % of actual levy to actual output from 1949 to 1952 for selected towns in southern Jiangsu

Source: Zhong (2005). No pagenumber

The actual grain levies (including local surtaxes) in southern Jiangsu increased annually.Using the 1949 actual levy as a baseline index of 100, the figures were 138 in 1950 and 176 in 1951. In terms of the percentage of actual levy to regular expected output, it was 14.27% in 1949, 19.44% in 1950, and 21.89% in 1951.

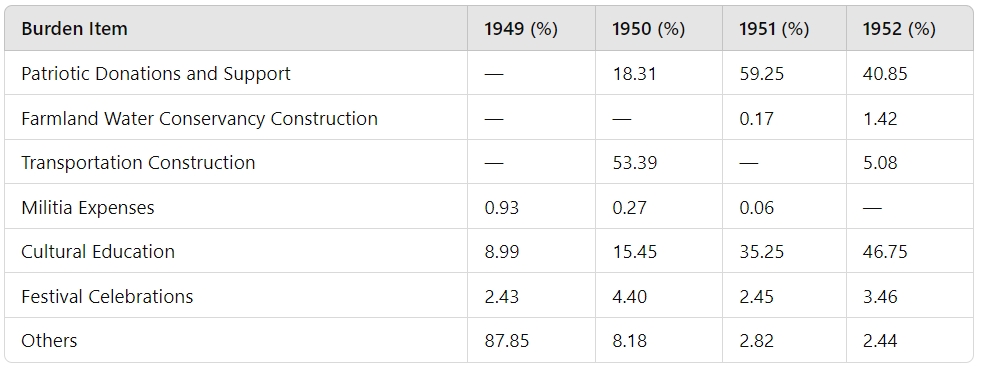

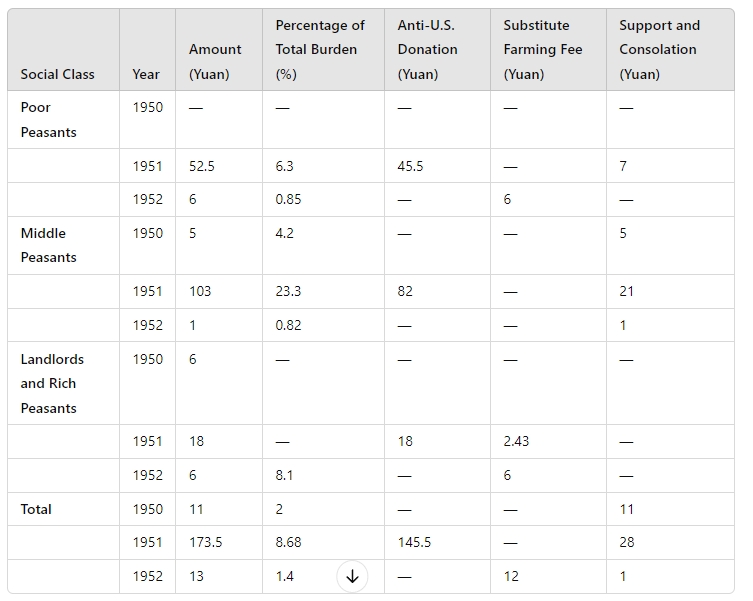

Farmers not only bore the agricultural tax burden but also additional miscellaneous charges such as patriotic donations and preferential support. Table 40.8 shows the proportion of various burdens for 25 households in Chaoyin Township, Wuxi, from 1949 to 1952.

Fig. 40.9 Proportional table of burden projects for 25 households in Wuxi Chaoyin Township from 1949 to 1952

Source: Zhong (2005). No pagenumber

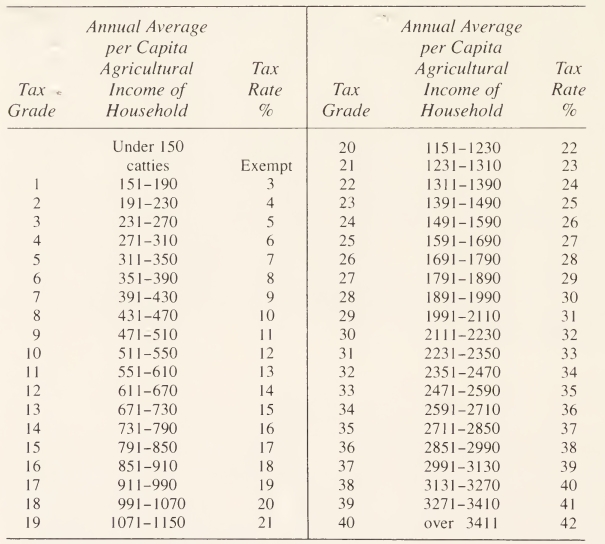

This table indicates that patriotic donations and support accounted for 18.31% in 1950, topped the miscellaneous burdens in 1951 at 59.25%, and were second only to cultural education in 1952 at 40.85%. The proportion of patriotic donations and support varied among different social strata; generally, middle peasants bore the largest share, followed by poor peasants, with landlords and rich peasants bearing the least. See Fig 40.14 Tax collection during the early 1950s presented a complex and multifaceted challenge. Variations were observed across different years and Regions, as well as in the implementation of tax regulations. Prior to 1952, the agricultural tax was theoretically collected based on a fixed base, although the specific rate differed annually, being adjusted according to the party's requirements. The determination of the "should-be normal yield" (Changnian yingchan liang) for each household's land involved a democratic discussion among peasants, taking into account factors such as the amount of cultivated land, soil fertility, planting practices, and average harvests. The locally ratified figure served as the basis for determining the portion of this base number that households paid in agricultural tax each year. The tax rate ranged from 15 percent to 25 percent, depending on the specific year. Interestingly, the actual crop yield played a relatively minor role in determining the amount of taxes paid by peasants. Consequently, regardless of the claimed high yields of their land, peasants were not obligated to pay more than the predetermined fixed amount.

Hou (2008) writes

"In the short term, fabricating a high yield would not cost peasants a penny; quite the contrary, if the unit yield was high enough to impress local cadres, local government was likely to reward peasants with a bonus, sometimes a draught animal or sometimes a expensive farm implement, which by no means were trivial. Furthermore, having their names known to local leaders could easily bring peasants a bunch of benefits, such as priority in obtaining government loans, being nominated as model laborers, etc. The model laborers would be provided chances to travel to the provincial capital, to Beijing, or even abroad." This changed in 1953. In 1953, the amount of tax was determined by the land owned by each family. The goal of this campaign “measure land area and determine production levels” was to maximize the amount of grain the government could collect from each peasant family.

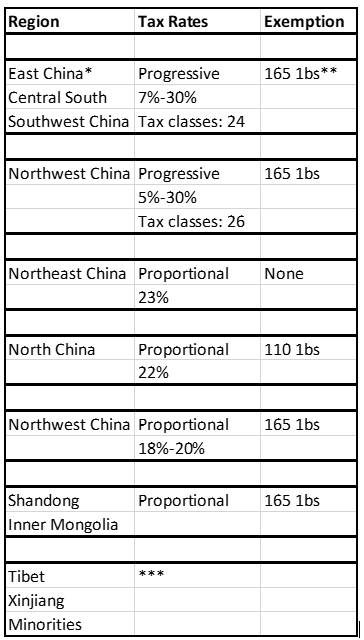

Fig. 40.10 Major features of agricultural taxes (1953)

Source: Chao (1957). Page 152 *Except Shandong ** local staple grain *** Rates to be determined seperatly"This movement hit the newly liberated Regions particularly hard where peasants tended to have hidden a large amount of unregistered land. Old liberated Regions such as north China and northeast China where land reform had been carried out rather radically and peasants had gone through a series of political movements, the impact of the “measure land area and determine production levels” movement on peasants was relatively moderate."

In 1952 all local surtaxes in the agricultural tax system are abolished. The reason was that in the early 1950s, surcharges on state taxes, particularly agricultural taxes, posed a significant problem in China. Initially, local surtaxes of up to 15 percent were approved, later increased to 20 percent in 1951. Township and village government spending had increased due to expanding government and CCP roles. A 1951 survey found that only a third of local government funds for various purposes came from the government budget, with local apportionments, donations, confiscation from landlords, business taxes, and revenue from local public businesses making up the rest. Additionally, informal exactions and 'voluntary' donations further burdened taxpayers. In some areas, miscellaneous charges reached as high as 560 percent of formal taxes. In 1952, the central government ordered the elimination of all surcharges and apportionments, addressing the issue of uncontrolled local extraction. However, financial constraints led to the decree being in force for only a year. Primarily, the tax aimed to incentivize the cultivation of specific crops such as cotton, tobacco, and hemp. Its broader goals included boosting overall production and cultivation, facilitating the redistribution of land from landlords to peasants, and promoting a fairer distribution of income among individuals farming their own land. As an incentive to increase the amount of land under cultivation, newly ploughed acreage was exempt

from the tax for a period of from three to five years.

Fig. 40.11 Revenue of the central government and local government from 1950 to 1954

Source: Du (2010). Table S6. https://www.mdpi.com/2071-1050/11/24/7027/s1

In early 1950, several regions in East China, especially newly liberated areas witnessed significant social unrest stemming from the CCP aggressive grain procurement policies. In the immediate aftermath of the revolution, the CCP encountered widespread resistance to its grain collection efforts. While initially attributing these disturbances to natural disasters and banditry, the Party later acknowledged the crucial role played by its own policies.

Excessive grain levies, often exceeding local capacities, proved to be a major point of contention. The implementation of policies like the "large household additional levy" in Jiangjin County, Sichuan, led to severe economic hardship and widespread resentment among the local population. Similar patterns emerged in regions like Guizhou and the broader Southwest, where the CCP's policies often triggered local unrest, sometimes mistakenly labeled as "bandit disturbances."

These incidents highlight the inherent tension between the state's need for resources and the realities faced by local communities and local cadres. The CCP, in its early years, struggled to effectively balance these competing demands, leading to significant social and economic consequences. Consequently, the rural cadres played essential roles in various aspects of rural governance, including agricultural tax collection, delivery of commodity quotas to state procurement agencies, and administration of other levies in rural areas. These cadres, often recruited locally and thus familiar with specific local conditions, families, and customs, formed crucial links in the chain of governance. Without their services, the CCP leadership would have faced significant challenges in swiftly consolidating the new order across the extensive rural periphery.

Unified Grain Procurement ...

Implemented in 1953, the policy of 'unified purchasing and marketing' granted the state exclusive authority to purchase and sell grain, and eventually other agricultural products, at predetermined prices and quotas. This initiative eliminated the intermediaries of the previous system and ensured affordable grain supplies for urban areas. State control over pricing and quotas effectively functioned as a covert tax by providing inadequate compensation to agricultural producers. See also Article 37

Tax paying

Initially conceived as a response to the state grain procurement crisis during the inception of the first Five-Year Plan in 1952-1953, this policy witnessed a significant surge in state investment in infrastructure, escalating from ¥4.35 million to ¥9.04 million. Consequently, there was a noticeable uptick in employment rates, with approximately 20 million laborers migrating from rural to urban areas. This demographic shift led to a reduction in agricultural production engagement among the Chinese population, while urban food demand surged by 9.3%, and non-agricultural population demand soared by 32%. During the period spanning July 1952 to June 1953, the state procured 27.35 billion kilograms (kg) of grain, whereas market demand stood at 29.35 billion kg, resulting in a deficit of 2 billion kg, which was offset by utilizing state grain reserves. In comparison to the preceding year, the proportion of national grain output allocated to state storage decreased from 28.2% to 25.7% in 1952-53. Furthermore, exacerbating the situation, Manchuria, historically known as the "granary" of the new republic, suffered a natural disaster resulting in a loss of 4 billion kg of grain. On September 4, 1953, grain merchants exhausted all flour stocks in both national and local markets, prompting shortages in Beijing and Tianjin. Consequently, the government was compelled to implement temporary rationing measures.

During the initial years, the central government did not impose restrictions on free markets. Instead, it acquired grain through the requisitioning of public grain and purchases from the open market. As the economy recovered and large-scale economic construction commenced, a growing disparity arose between state-controlled grain reserves and the amount required to supply urban and rural areas. Between 1949 and 1952, as the state gradually assumed a dominant regulatory role in grain trade, purchases and sales continued to operate beyond the realm of government planning. The period saw fluctuating grain output, leading to variations in supply and demand, and opportunistic behavior causing spikes in grain prices. To promptly address this challenge, the GAC issued the Decision on the Implementation of the Planned Purchase and Planned Supply of Grain in November 1953, after thorough inquiries and discussions. The directive outlined that the actual amounts of grain purchased and supplied, available for sale to grain-short peasant households, would be determined based on the country's and people's needs and the village's actual situation. Administrative areas received quotas from the GAC Finance and Economics Committee, with larger regions determining quotas for their subordinate levels. Quotas for sub-districts and xiang (or cun) were set by the county. These quotas underwent democratic discussions, and local adjustments were allowed. Suggestions for alterations were proposed by lower-level cadres, passed to superiors, then conveyed to provincial officials, ultimately leading to a revised draft plan subject to approval by large administrative-area officials.

One side effect of introducing UGP has to be mentioned.

" Timing the introduction of Unified Purchase to coincide with the harvest, then, dealt a double blow to grain dealers: it not only cut off all their

future business, but also tended to penalize them for speculative activity during the year just past."

There was a second side effect. The rapid infusion of funds from the state's grain monopoly destabilized rural finances, sparking high-interest loans, hoarding, and black market operations. Local authorities, showing a mature understanding of currency surplus risks, reacted with policies that effectively served as monetary controls.

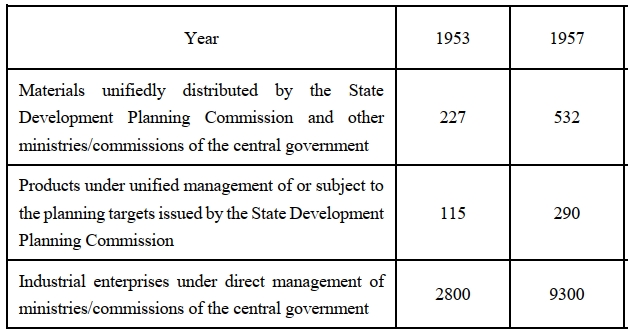

Fig. 40.12 Quantity of Materials Managed and Distribute by the Central

Government and Number of Industrial Enterprises under Direct Management of the Central Government

Source: Research team (2019). Page 57

In 1957, central planning in China saw a significant expansion compared to 1953. Specifically:

Material Distribution: The State Development Planning Commission and central departments distributed 532 types of materials, representing a 134% increase.

Planned Products: The number of product types under unified management or with direct planning targets reached 290, a 152% rise.

Industrial Enterprises: The number of industrial enterprises directly managed by central government departments surged to 9,300, marking a 232% growth.

Unified Purchase and Sale: Essential commodities like grain, edible oil, cotton cloth, and cotton were incorporated into the unified purchase and sale system. In November 1953 a nationwide implementation of planned purchases of oil bearing materials was also introduced. In September the following year, the GAC issued the Order on the Implementation of the Planned Acquisition and Planned Supply of Cotton Cloths. The government categorized all agricultural products into three groups based on their significance in people's lives and economic progress. The first category encompassed essential items such as grain, edible oil, oil-bearing crops, and cotton. The second category comprised significant animal products, tea, silk, and sugar. The remaining agricultural products were placed in the third category. Distinct institutional arrangements were established for each of the three categories within the marketing systems. A tiered system governed agricultural goods. The second tier, encompassing meat, seafood, tobacco, tea, silk, and sugar crops, was subject to mandatory government purchase. Producers faced fixed procurement quotas and prices, but could sell surplus on the free market. The third tier, primarily vegetables, fruits, and some industrial crops, lacked mandatory quotas. However, restrictions on long-distance trade gave government agencies significant market control, particularly over industrial crops, enabling them to influence prices. Labor Deployment: All unit labor was included in the labor deployment plan.

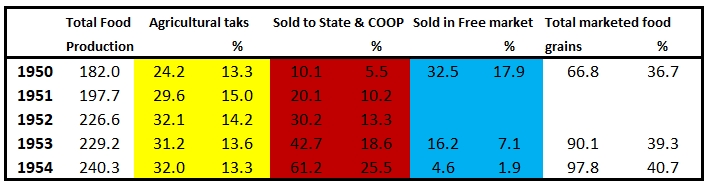

Fig. 40.13 Marketed ratio of food grain 1950-1954

Source: Ishikawa (1967) Page 41 in billion catties of hsi-liang The liang is a traditional Chinese weight unit. In modern China, the liang equals 1/10 jin or 10 qian; this is exactly 50 grams (1.7637 ounces).

Rural residents were compelled to sell everything to state stores, with no market sales allowed. Urban citizens had limited market access for items like poultry and eggs, but this could be revoked by provincial authorities. The UGP's implementation was immediately followed by a surge in suicides, with 262 cases in Sichuan province alone in the first month

Urban areas initially embraced the UGP with favor. Food supplies, encompassing grain, sugar, cooking oil, and meat, were distributed in cities through rationing based on criteria such as age, gender, and physical work involvement. Despite the austere nature, most urban residents received a sufficient and satisfactory food supply, leading to the characterization of the UGP as a necessary and appropriate policy.

Problems ...

The issue of hidden land posed significant challenges to central planning and control, but it was not the sole obstacle in local tax administration. Safeguarding grain storehouses emerged as another critical concern in the newly liberated regions. The burning of public granaries, particularly in the months following liberation and continuing sporadically into 1951, was a common tactic employed by counterrevolutionaries, disgruntled villagers, bandits, and vandals. This aimed at both stealing supplies and intimidating peasants cooperating with the revolutionary government.

To counteract these threats, People’s Militia units were formed to protect granaries and law-abiding villagers. However, security measures were not consistently enforced, resulting in unnecessary losses. Despite efforts by the central leadership to establish comprehensive reporting systems for public grain, the shortage of local cadres proficient in calculations and accounting led to discrepancies in reported grain amounts.

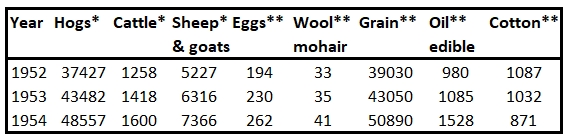

Fig. 40.14 State procurement of selected crops, live animals and livestock products

Source: Crook (1988) Pages 70-71 *1000 head ** 1000 tons

Many of these cadres lacked experience in inspecting and evaluating grain quality. Peasants, not always sending their best grain to tax collectors, often delivered improperly dried or infested grain, which went undetected by granary cadres, leading to its storage alongside good grain. Black market trade in grain did crop up in many areas and there were numerous reports of illegal private trade in grain even after UPG was well under way.

Corruption among new local cadres further exacerbated the situation, with some accepting bribes to lower tax assessments, misappropriating public grain for personal use, or engaging in private lending at exorbitant interest rates.

Furthermore, village cadres, involved in concealing their own land, were also complicit in helping fellow villagers hide land, sometimes in an attempt to curry favor and deceive the government. These multifaceted challenges underscored the complexity of local tax work and posed obstacles to effective governance.

During the protest of peasant against UPG, cadres tended to accentuate the so-called “class line” by linking rural residents’ attitudes towards state policies to their class status, and distinguishing poor and middle peasants from their “class enemies” or landlords and, to some degree, rich peasants.

The notion of social hierarchy and "class struggle," solidified during the land reform of the early 1950s, began to lose relevance during the grain procurement campaign. Local resistance predominantly stemmed from ordinary peasants and local cadres rather than the previously targeted "class enemies" who were dispossessed and intimidated. The diminishing applicability of the "class line" ideology, observed in both affluent and impoverished regions, contributed to the state's eventual shift towards a more pragmatic approach to rural unrest, which became evident a few years later during the cooperativization process.

By the close of 1954, there were indications that central planners were recognizing an overall excess in purchases. The grain quotas issued from higher authorities had absorbed a significant portion of the peasants' surplus, leading to a growing undercurrent of dissatisfaction and apprehension. Central authorities were increasingly alarmed by the implicit threat from peasants to intentionally reduce production in the upcoming year. Reports from regions such as Hunan and Hubei highlighted instances where numerous peasants were purposefully neglecting to apply fertilizer to their rice fields and adequately prepare them for cultivation. In order to mitigate resistance from farmers, significant emphasis was placed on cadres to adopt appropriate working methods and tactics. Nevertheless, in certain areas, extreme measures were employed to enforce the UGP. The government dispatched work teams to rectify these radical practices. Challenging the UGP was deemed unacceptable, as it was perceived as an act of rebellion against the CCP.

Article 9 of the Decision of the GAC on the Implementation of the Planned Purchase and Planned Supply of Grain states "Anyone who violates these regulations by speculation, disrupting the market, spreading rumors and sabotage must be dealt with strictly."

Other taxation...

Before establishing the national regime, the CCP implemented alcohol monopolies in their controlled areas to reduce alcohol consumption, preserve grain for food, and supplement military income. In January 1951, the Ministry of Finance conducted the first national monopoly conference, confirming the monopoly management system for alcoholic commodities. In May 1951, the Ministry of Finance issued Provisional Regulations on Monopoly to unify the management of the national alcohol monopoly. The government aimed to capitalize on the high alcohol consumption rate to generate significant tax revenue for national development. By monopolizing alcohol, the government sought to regulate production based on grain availability, ensuring a sustainable food supply.

The PRC never taxed wages, although there were large differentials in the 1950's. No inheritance tax has ever been established.

The tax reform in 1953 was implemented to accommodate the new China’s FFYP.

"Specifically, in 1953, the taxation system was revised to introduce the commodity circulation tax, to abolish the special consumption tax, and according to the tax items, to incorporate them into the business tax and the newly established culture and entertainment tax. In addition, the business tax and goods tax were adjusted accordingly." The taxes, which remained:

Commodity circulation tax , Commodity tax , Industrial and commercial business tax , Salt tax , Custom duties, Agriculture tax, the Industrial and Commercial Income Tax, Stamp tax, Slaughter tax , Urban real estate tax , Cultural entertainment tax , Vehicle and vessel license tax and, Interest Income tax.

Import tax...

Between 1949 and 1950, the CCP Military Control Commissions took control of eighteen major maritime customs offices, initiating a gradual phase-out of foreign staff and mandating Chinese language documents. The establishment of the General Administration of Maritime Customs in late November 1949 brought significant changes in tariffs, regulations, and goods inspection. By 1951, the Chinese Government issued its first national maritime customs code and tariff regulations. The takeover process extended to cargo surveys and measurements, with the establishment of the Tianjin Bureau of Inspection and Testing of Commodities in April 1949. A subsequent order mandated the cessation of private adjuster firms, transferring inspection and marine measurement functions exclusively to the Government Bureau. Some foreign firms were affected, while others, like a Swiss firm, were allowed to continue their activities privately.

On January 27, 1950, the GAC issues the policy regarding customs in accordance with the following goals:

a. The supervision and control of customs work and foreign trade activities should have important effects on the recovery and development of

the people's economy.

b. The customs tariff must protect production and safeguard the competition of domestic products with foreign merchandise.

c. The Customs Administration must be a centralized, unified, independent and autonomous organ of the State. The Customs Administration shall be responsible for the direct supervision and control of the import and export of various commodities and currencies, the collection of customs duties, and the prevention of smuggling, in order to insure that China will not again be subject to economic aggression by capitalist countries.

d. With respect to manufactured and semi-finished goods that can be produced in large quantities domestically and such goods that potentially can be produced in the future, the import tariff for such goods should be higher than the difference between the cost of such goods and the cost of similar domestic products in order to protect the national industry.

e. With respect to luxury goods and nonessential goods, the import tariff should be even higher.

f. With respect to equipment, machinery, and materials for production that cannot be produced or cannot be produced in sufficient quantities domestically,

and with respect to industrial raw materials, agricultural machinery,foodstuff seeds, and fertilizer, there should be either low duties or none at all.

g. In order to promote the production of such goods for export, there should be very low duties for all semi-finished goods and industrial materials, or

in some cases, no duties at all. See also Article 37

Bonds...

In December 1949, the introduction of “People’s Victory Real Unit Bonds” took place. The interest rate was to be 5%. These bonds were to be repaid over a period of 5 years ending in 1956. On January 1, 1950, 100 million real units were issued. The issue of bonds was considered much more preferable than raising taxes. The sales campaign explicitly aimed at private industries, wealthy people, and retired GMD officials.

Bonds

The imposition of bond-buying quotas, coupled with concerns about taxes, created distress among businessmen. The municipality and its subdivisions, along with private institutions, faced quotas, leading some less-favored entities to sell assets to meet their bond subscriptions. Publicizing individual and organizational subscription amounts aimed to shame and pressure people into increasing their contributions. Despite efforts to evoke empathy and competition, compulsion became evident, with many individuals jailed for failing to meet forced quotas. By the end of July, only seventy-four percent of the total quota was raised, prompting the cancellation of a planned autumn bond-buying campaign by the government.

There were no reported bond issues from 1951 through 1953. From 1954 through 1957 the government floated each year so-called “National Economic Construction Bonds.”

Fig. 40.15 Disrtibution of domestic bonds 1950 and 1954

Source: Prybyla (1970) Page 210

* in thouands of yuan

Leighton (2014). Pages 128-129 "During the summer of 1949, his (Gu Zhun, a tax administrator) duty to nurture local finances clearly came second to funding a fledgling regime still fighting a civil war. Despite the difficulties Shanghai faced even through that grim time, it provided a quarter of national tax receipts—more than any other region. Shanghai was, as Chen Yun put it, “worth five Tianjins.”16" Page 127 Chu (2023). "When the CCP took over cities in 1949, it also remained most preexisting taxes and surcharges. In the cities of Zhangjiakou and Xuanhua, the new government announced the abolishment of six kinds of taxes while keeping the remaining twenty-seven in effect.45 This announcement also stated that this tax collection approach should be a prototype for other cities occupied thereafter.46 The Communist Military Government in Tianjin and Shanghai also announced that “all existing national and municipal taxes will continue to be collected.”47" Page 19 [↩][Cite]

Xue (2023). Page 21 [Cite] "Accountants’ work in the early stages seems to have been very simple, often seen as similar to statistics, suggesting that accounting was reduced to mere bookkeeping. Anyone with a bit training could be an accountant." Page 16

Mao Zedong writes in december 1942 "(4) The Border Region Government and the governments of all the counties should seek out students educated to the upper primary school or higher level for training as accountants or managers so as to ease the difficulties of all cooperatives over these." 00-12-1942 Mao Zedong Economic and financial problems in the anti-Japanese war. 5. On the development of cooperatives Mao Zedong writes on accounting "Establish the system of economic accounting [jingji hesuanzhi] overcome the muddled situation within the enterprises. To achieve this we must do the following. First, each factory unit should have independent capital (liquid and fixed ) so that it can handle the capital itself and its production is not frequently hindered through capital problems. Second, income and expenditure in each factory unit should be handled according to fixed regulations and procedures, putting an end to the confused situation where income and expenditure are not clear and procedures are not settled. Third, according to the actual situation in the factories some should adopt the cost-accounting system [chengben kuaijizhi] and some need not for the time being. However, all factories must calculate costs. Fourth, each factory should have regulations for inspecting the rate of progress in completing the annual and monthly plans. They should not let things slide by doing without inspections for long periods. Fifth, each factory should have regulations for economizing on raw materials and looking after tools, and for fostering the practice of doing these things. All these points are the chief elements of the system of economic accounting. Once we have a strict accounting system, we can examine fully whether an enterprise is profitably operated or not."

00-12-1942 Mao Zedong Economic and financial problems in the anti-Japanese war. 7. On the development of self-supporting industry [↩][Cite]

Wen (2021). Pages 43-44 [Cite] Li (2019). Besides,there was also a food issue, feeding for example, two million GMD and PLA officers and soldiers was among the most pressing and immediate burdens on the local government in Sichuan and there was the need to extract vast amounts of grain for military expeditions to Tibet. Page 131 [↩][Cite]

Bays (1969). Pages 39-40 [Cite] Shue (1980) remarks "The first tax collection in 1949-50 was, by the government’s own admission, rather a crude affair; no official tax regulations were yet in effect for these areas. The army did much of the work, however, and the general principle observed by PLA details and tax collection work team cadres was apparent enough. They seized as much as they could from the obviously wealthy, resorting, when they had to, to coercion. They always tried to give the most poverty-stricken and destitute households total exemptions. And for the majority of households falling somewhere between these two extremes, they set a figure significantly below the previous KMT levies and granted many petitions for special consideration." Page 30 [Cite] 28-04-1950 Mao Zedong On Opinions Regarding Spring Plowing, Land Reform, Cadre training and selling bonds[↩]

This applied to 22 categories of key commodities, including tobacco products, alcoholic beverages, flour, matches, cotton thread, paper, cement, pig iron, nonferrous metals, rolled steel, coke, and others. The tax imposed only once in the production stream and was generally paid by the wholesale commercial organization upon receipt of the goods, or by the producer in case of a direct sale bypassing wholesalers. [↩]

Wang (2001). "The retained personnel were relatively well educated (all had at least junior high education and some had college degrees) and were experienced. Many, however, were corrupt, since accepting bribes and colluding in tax evasion were common in Nationalist-era Wuhan. Moreover, many of these holdovers were not fully supportive of the new regime. In contrast, the Communist cadres assigned to the agencies were dedicated to the new regime and had not been corrupted but generally lacked formal education and tax collection experience." Page 242 [↩][Cite]

Wang (2001). Page 255 Even before these campaigns, measures were taken to improve the work of taxation. See for example RMRB 28-03-1950 The Central Administration of Taxation formulates measures to regularly reward and punish tax staff to ensure the implementation of tax policies and improve work efficiency [↩][Cite]

Like the blades of a pair of open scissors, the prices of industrial and agricultural goods diverged, reaching a peak in October 1923 in the Soviet Union where industrial prices were 276 percent of their 1913 levels, while agricultural prices were only 89 percent. This meant that peasants' incomes fell, and it became difficult for them to buy manufactured goods. As a result, peasants began to stop selling their produce and revert to subsistence farming, leading to fears of a famine. https://en.wikipedia.org/wiki/Scissors_Crisis Bernstein (2003). "Now (1953), the state, through the collective system, controlled the harvest and decided not only the amount of the tax (gongliang) but also how much surplus grain yuliang) had to be sold to the state at state-determined prices, often lower than market price. 63 Conversely, high state-set prices governed the sale of industrial goods to the countryside, creating a scissors effect from which the state profited greatly. All this was done through the national unified procurement and marketing system through which the Maoist state massively transferred resources from the countryside to the urban sector. Much of the largest burden placed on the peasantry thus did not come in the form of taxes as such but in the form of the compulsory procurement program." Page 36 [↩][Cite]

Fig. 40.15 contributions made by different social classes in Group Five of Zhankou Township, Yixing County, from 1950 to 1952

Source: Zhong (2005). No pagenumber

This data indicates that during the Movement to Resist U.S. Aggression and Aid Korea, farmers were compelled to contribute a significant portion of their limited grain and resources to meet agricultural taxes and miscellaneous patriotic donations. Farmers generally complained about the heavy burden. Especially in disaster-stricken and hilly areas, many farmers experienced 'running out of food after paying public grain.'"

[↩][Cite]

Hou (2008). Pages 104-105 Shue (1980) states "The Party appears never to have seriously considered the alternative

of applying the agricultural tax to the individual. To understand why, it should first be noted that the Chinese tax did not apply to the value of the land an individual owned: it was the harvest or income derived from the land that served as the tax base.10 The Chinese tax was a tax on output or production, not on possessions or property. In such a system it is reasonable that the tax should be applied to the production unit rather than to the individual peasant, landowner, or proprietor as such. And in China in 1950 the basic agricultural production unit was indisputably the farming household." Page 108 [↩][Cite][Cite]

Li (2019). "In Hechuan County (Sichuan), the government implemented a levy on grain five times in three months, including the annual levy, the additional levy, the supplement levy, the expanded levy and the special levy." Page 150 [↩][Cite]

Gao (2013). "Communist food rationing was not an urgent economic policy designed because of famine or war. It was designed in 1953 to ensure grain supplies for a growing urban population and to support the country’s industrialization programs. In most years, after they paid agricultural tax in grain, farmers did not have much food left,39 but the government demanded more and more from them to feed people in the cities, and bureaucrats started falsifying records and forced farmers to sell all “surplus” to the state, which caused periodic famine and food shortage in rural areas." Page 269 [Cite] and Gao (2010). [↩][Cite]

Li (2019). The primary clientele of state-owned grain trade enterprises consisted of private merchants. These merchants procured grains wholesale from state-owned grain trade enterprises in production areas and then transported them to urban centres for retail sale. Their retail pricing was determined by the wholesale rates set by state-owned grain trade enterprises, and they would actively engage in transportation and sales if they could profit from the price differentials offered by these enterprises. The relationship between the CCP and these merchants was not consistently adversarial; at times, it was even cooperative. In August 1951, the State-owned Grain Trade Enterprise of East Sichuan issued a provisional regulation encouraging private merchants to assist in the procurement and sale of grain for the state-owned enterprises. Page 230 Li (2019) cites a document of the Eastern Sichuan State-owned Grain Trade Enterprise "It is not the goal of our business development to let private merchants act as our purchasing and sales agents, [but] it is a transitional method for temporarily conducting business as we have not yet set up any organisations, our cooperatives and retail enterprises have not been established.28" Page 231 [↩][Cite]

Perry (1985). "...Changjiang ribao had reported on riots by Hubei peasants in protest against the state's handling of the grain purchase programme.16 In (29) November 1951 People's Daily published a self-criticism by the Hubei Provincial Committee which admitted to serious problems in the implementation of land reform and collection of agricultural taxes.17" Page 419 [↩][Cite]

Liu (2019) gives an example from Northern Jiangsu "The agricultural output dropped by 30-40 percent in 1949, causing a desperate shortage of food across the region. To make it worse, farmers had to pay grain tax which normally amounted to 26 percent of their annual harvest; for some middle farmers, the tax could be as high as 30 percent. Consequently, many farmers who were unable to sustain their lives requested the government to lend them rice, but their pleas were always rejected by local cadres. Irritated by the indifferent attitude of government officials, the hungry farmers finally decided to obtain food by force. Unlike in the famine of spring 1946, however, their targets this time were the state granaries instead of landlords’ storerooms, because even landlords were also short of food. As a result, around 9 p.m. on January 11, 1950, about 1,300 villagers from Longwei Xiang of Yangzhou Prefecture gathered before two state granaries. In harsh whistles and gongs, they beat up cadres, burst open the doors, and looted the granaries. ...Unexpected to these farmers, however, they soon found armies were sent in to force the recovery of the looted granaries" Page 332 [↩][Cite]

See for example RMRB 07-03-1954 Political and legal departments should ensure the implementation of the unified grain purchasing and marketing policy [↩]

Pomp (1981). "...was introduced in 1953 and appears to have been modeled after a similar tax in the Soviet Union. Twenty-two categories of goods were subject to the tax and exempt from all other taxes. ...the rates of tax ranged from 7% to 66%, and that they were applied to the state price of the taxable good." Page 17 [↩][Cite]

Pomp (1981). "...was introduced in 1950. Producers or wholesale buyers paid the tax, and the rates ranged from 3% to 120% of the wholesale price of the good. ...Industrial goods generally were taxed at lower rates than consumption goods. Within the latter class, necessities generally were taxed at lower rates than luxury goods." Page 18 [↩][Cite]

Pomp (1979). Page 6 "All industrial and commercial profit-making enterprises within the boundaries of the People's Republic of China, whether State-owned, privately owned, part State-owned and part privately owned, or cooperative are subject to the income tax.6...Though the ICITA refers to street peddlers and poor craftsmen,21 in practice no individual, even street peddlers and poor craftsmen,is subject to the income tax.22." [↩][Cite]

Pomp (1981). "The amount of the salt tax, which is levied on a tonnage basis, varies from region to

region. The tax ranges from under 100 yuan per ton to 160 yuan per ton and is paid by the producer." Page 16 [↩][Cite]

Tax imposed on all documents used in commercial transactions and in the transfer of property. Land deeds during the land reform are exempted [↩]

Pomp (1981). "The slaughter tax is levied at the time of slaughter at a fixed amount per animal.

The amount of tax, which is different for each animal, is based on the animal's fair market value. The tax is paid to the local government by the owner of the animal. An exemption is provided for the slaughter of animals during specific holidays." Page 15 19-12-1950 Provisional regulations on Slaughter Tax of the People’s Republic of China[↩][Cite]

Pomp (1981)."The real estate tax is levied only in the cities and is a source of local revenue. The rate of the tax varies from one city to another." Page 14 The tax is divided into two categories, the housing property tax and the land property tax. [↩][Cite]

Pomp (1981). "The vehicle license tax applies to all vehicles, but some cities exempt nonmotorized vehicles such as carts and bicycles. Beijing, for example, exempts bicycles owned by Chinese. The tax is paid once a year to the local government, with proceeds earmarked for road construction. The tax does not appear to be levied in the rural areas. The amount of the tax varies. In the case of motorized vehicles, which generally are not owned by individuals, the tax is based on tonnage. For other vehicles, the tax is a fixed amount." Page 15 [↩][Cite]

Pomp (1981). "In 1950, an interest tax was instituted on interest from bank deposits. Beginning in December 1950, the tax was broadened to include interest from bonds, securities and loans to employees. The tax rate was a flat 5%." Page 43 [↩][Cite]

RMRB 31-01-1951 "The Central People's Broadcasting Station is scheduled to broadcast the winning numbers of the first phase of the 1950 People's Victory Realized Public Bonds from 8:15 to 8:30 pm on February 1. People's Broadcasting Stations in various places will broadcast the winning numbers." [↩]

Skinner (1951). Page 72 "(February 12, 1950) A serious riot by 20,000 textile workers against Communist authorities took place in Shanghai last month. It followed a wage cut and an announcement that the customary annual bonus paid by the China Textile Company would be converted to people’s bonds." The Militant, 20 february 1950 Page 1 "Stalinist rulers brutally suppress Shanghai workers" [↩][Cite]