Currency and Banking: Financial enterprises shall be strictly controlled by the state. The right of issuing currency belongs to the state. The circulation of foreign currency within the country shall be prohibited. The buying and selling of foreign exchange, foreign currency, gold and silver shall be handled by the state banks.

Private financial enterprises operating in accordance with the law shall be subjected to supervision and direction by the state. All who engage in financial speculation and undermine the financial enterprises of the state shall be subjected to severe punishment.

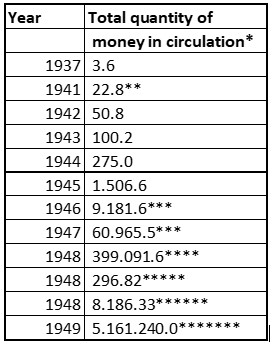

In 1949, the new regime inherited a colossal hyperinflation from the GMD regime. The GMD had tried to stop this inflation by introducing two times fiat paper money. Both times the interference failed. Both currency had lost more than 99.999% of their initial values. The Fabi (法幣 "Legal tender") existed for 13 years, the Gold Yuan only 10 months. In 1935, when the silver standard was suspended, Fabi was introduced. (The circulation of silver dollar coins was prohibited, and private ownership of silver was banned.) In 1948, the Gold Yuan replaced the Fabi and all use of foreign currency was declared illegal. The gold yuan was nominally set at 0.22217 g of gold. However, the currency was never actually backed by gold, and hyperinflation continued. In a last attempt to stop the inflation the Silver Yuan was introduced in 1949.

Fig. 39.1 Inflation

Source: Wang Hongsong (2020). Page 564

* the total quantity of money in circulation (currency and demand deposits) in billion yuan

**December 1941

***December 1946 /1947

****July 1948

*****August 1948 introduction of Gold Yuan

******December 1948

*******April 1949

Due to its rapid depreciation, Gold Yuan was effectively taken out of circulation and replaced by silver, foreign currencies and goods-for-barter in July 1949.

In December 1948, the People’s Bank of China (PBC) issued the Renminbi (Chinese Yuan) in the Northern regions, which was fiat money. The CCP undertook a different approach to control inflation. The resilience of the new currency against inflation did not stem from a planned system, but rather from the state's capacity to link the value of the renminbi to a selection of vital commodities under the control of state commercial and industrial entities. This innovative approach was primarily drawn from the Communists' prior economic challenges in predominantly rural agrarian regions during revolutionary campaigns, notably in pre-1945 Shandong and the Manchuria area throughout the Civil War.

Currency

The PBC was founded in Shijiazhuang of Hebei Province on December 1, 1948 , by merging three Communist-controlled Regional banks namely, the Northeast Bank, the Northern Sea Bank, and the Northwest Farmers Bank into a single bank. The predecessor of the PBC was the National Bank of the Chinese Soviet Republic established by the CCP in November 1931. By the close of World War II, in 1945, nineteen “Liberated Areas” had been created in Shaanxi, central and south China. These banks were totally independent one from the other due to their obvious geographic and economic separation. The PBC sought advice from foreign and former GMD financial experts. The majority of office workers were employed before 1949 and were integrated into the new People's Bank primarily hailed from urban areas. They were averse to the prospect of being assigned to establish a new branch office in a small town. Additionally, a significant portion of these individuals had only been retained in their positions due to the critical nature of their expertise and experience, rather than being considered politically reliable elements.

The PBC became the bank for issuing currency, making monetary policy, and granting short-term credit and loans to both public and private commercial enterprises after 1949. In 1953, the State bank charged different interest rates on loans. State industrial enterprises were charged 0.45 -0.48%; State commercial enterprises were charged 0.69% and agricultural collectives 0.75%. The interest rate differential between agricultural loans and loans to state enterprises constitutes a state subsidy to industry through its monetary policy. However, in 1955, the rate of loans for agricultural collectives decreased to 0.60%. The old Bank of China became a joint state-private bank. Nan Hanchen became the new president of the PBC from December 1948 to September 1954.

A smooth takeover of the branches of the Bank of China was made possible because several employees had joined the CCP and protected the bank properties.

Much to the dismay of the Nationalist government, the Bank of China's Hong Kong branch retained its significant capital reserves while awaiting the establishment of the new government. Upon learning that Chiang Kai-shek had instructed the transfer of all national art treasures and funds to Taiwan, the manager of the Hong Kong branch, Zheng Tieru, swiftly allocated most of the bank's capital to real estate and local businesses. These investment endeavors effectively prevented the GMD government from relocating the branch's capital to Taiwan. The decisive actions taken by the Hong Kong branch exerted a strong influence on other overseas branches, prompting them to acknowledge the legitimacy of the new government. By advocating for the recognition of the People's Republic of China, the Hong Kong branch rapidly restored its business operations.

Currency

The conversion rate between Renminbi and the Gold Yuan was 1:100,000. The adaptation of the new currency proceeded smoothly, because the Gold Yuan had lost value and credibility. Within a week 53% of the total amount was changed and destroyed.

There are several factors contributing to the GMD's failure to stabilize its currency. Firstly, the GMD faced challenges from both the CCP and warlords who resisted surrendering their authority to the central government. By the middle of 1949, the government only had control over the areas surrounding Shanghai and a few other major cities.

Secondly, the GMD's intervention in mainland banks, particularly its involvement in bond trading and currency issuance, was not geared towards promoting economic growth. Instead, it primarily aimed at increasing government revenue for extravagant military campaigns. It was alleged that proceeds from bond sales were used for various purposes including provisioning troops, purchasing weapons, securing loyalty from military personnel, and enriching Chiang Kaishek and T.V. Soong's personal coffers.

Furthermore, widespread corruption became entrenched within the system, leading to a lack of skilled and motivated civil servants capable of formulating and implementing effective economic policies. The Central Bank failed to function as a typical central bank, lacking the capacity to provide professional guidance and tailored services to key industries or specific economic sectors.

CCP and inflation...

At the end of 1947, the CCP was capable of keeping the values of its currencies stable. The GMD regime, as seen above, had less control. The main instrument of the CCP was to minimize private speculations. The authorities, in the CCP controlled areas, kept the daily necessities at low prices by dumping materials from state stores into the free market. However, bureau officials quickly realized the drawbacks of this approach when they found that speculative funds were unexpectedly more adaptable and readily mobilized compared to physical materials. Recognizing the need for a shift in strategy, Harbin Trade Bureau officials sought a solution in the latter part of 1947 by bypassing the market through direct dealings with rural households facilitated by the CCP's influential grassroots organizations. In a typical scenario involving cotton cloth, procurement agents in Harbin simply provided rural women weavers with raw cotton materials and later collected the finished products directly from them, ensuring a cost-effective supply chain.

Finance

This policy meant controlling both raw materials and finished products and, consequently, decreased private trade.

However, the situation in Shanghai was complicated, the renminbi replaced the Gold Yuan, (the Silver Yuan could not be exchanged for renminbi) but the replacement of silver, gold and foreign currencies proved more difficult. The renminbi lost within 2 weeks 91% of its value of silver coins and prices increased by 170%. Speculation severed the situation. On 10 June 1949, the Shanghai Exchange closed. Speculators changed their targets to materials (grain, coal, and cotton). The CCP stroke back, they transported grain and cotton from all controlled areas to the major urban markets.

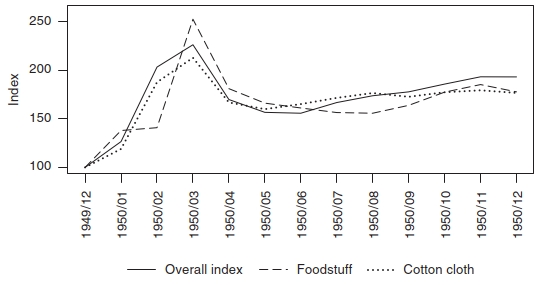

Fig. 39.2 Price Index People’s Republic of China, December 1949 to

December 1950 (December 1949=100)

Source: Weber (2021). Page 82

"...in April 1950, hyperinflation gave way to a decrease in the general price level, followed by renewed but less severe inflation with the outbreak of the Korean War in June.17 This general price movement closely corresponded with that of cloth and foodstuff, reflecting the CPC’s price-stabilization strategy focused on essentials."

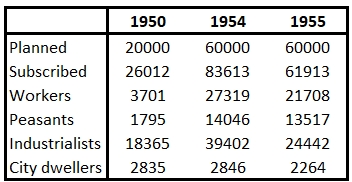

This measure halted speculation, leading to price stability by the end of March 1950. Additionally, the energetic promotion of bond sales seemed to have covered over half of the budget deficit in the initial six months of 1950. While private sector participation in bond purchases may not have been entirely voluntary, with businesses reportedly being compelled to subscribe to their full financial capacity, resorting to selling goods at discounted prices or below cost emerged as a last-ditch effort for most businessmen to raise funds.

Fig. 39.3 Amout of bond issue (planned and actually subscribed)

Source: Yin (1960). Page 87. Unit: 10000 yuan Gao (2004) states that the state blamed the merchants for Shanghai’s inflation, using the anti-merchant sentiments that existed in Shanghai. Merchants were labelled as ‘counterrevolutionaries’ or ‘evil speculators’. However, the main cause of the inflation was that the new administration issued too much paper currency because there was a huge fiscal deficit. In 1949, government revenue was 30.3 billion jin of grain, while its expenditure was 56.7 billion jin of grain.

While the new currency gained traction in urban markets, exchanges in rural areas of central and southern China continued to rely predominantly on silver coins and alternative forms of currency, with some remote markets reverting to barter trade. For the renminbi to establish itself in these regions, it needed to penetrate the rural market during its initial months. In many areas, party committees dispatched numerous work teams to persuade peasants to transition from using primary goods and silver coins to adopting the renminbi. Military of the Fourth Field Army bought necessary goods at low prices in the north and deposited the goods at state-owned stores in the south. The logistic department of the PLA bought these goods with renminbi to convince the farmers to follow suit. The policy of anti-speculation and price stabilization could only be a success if excess cash was reduced. The primary goal was to shift cash into deposits, particularly long-term fixed deposits. The National People's Bank supported the Cooperative's endeavors in Unified Purchase (as outlined in Article 38) by offering peasants preferential interest rates when depositing funds earned from selling excess grain to the state. These rates were quite appealing: 1.5% per month for deposits lasting one or two months, and 2% per month for deposits ranging from three to six months. The maximum term for deposits was set at six months, and only proceeds from grain sales were eligible for deposit.

The years when agricultural institutions' agricultural loans were larger than agricultural deposits were 1952-1956.

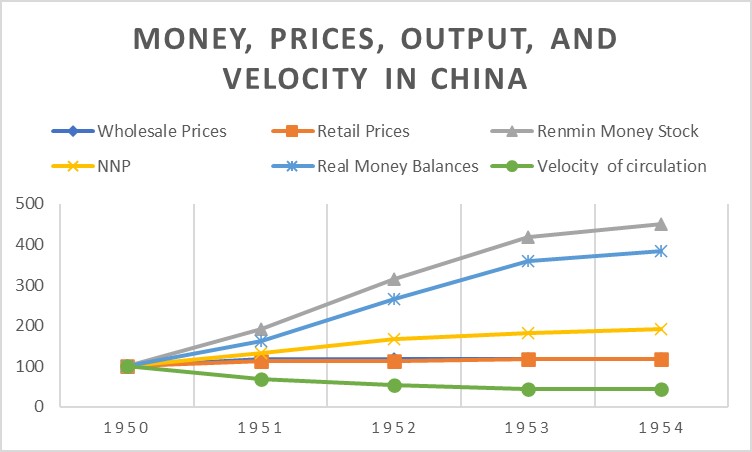

Fig. 39.4 Velocity Index

Source: Burdekin (2008). Page 59 Money stock: the total volume of money held by the public at a particular point in time. NNP Netto national Product Real money Balance measure the purchasing power of the stock of money. The index is 100.

This velocity indicates the average frequency with which currency exchanges occur throughout the year. With each exchange and expenditure of currency, additional upward pressure is exerted on prices. Therefore, an increase in velocity intensifies the situation where there is an excess of money chasing a limited supply of goods, exacerbating the issue further.

One remedy to solve the problem of rapid velocity was the introduction of the ‘parity deposit system’, the deposits were indexed to consumption commodities used by the local consumers. In May 1950, the monetary authorities introduced this new scheme of saving deposits; the deposit would increase in money value if the composite price of the real unit should increase, but would retain their original cash value if the composite price of the real unit should decrease.

On February 1, 1951, the People's Bank of China released a directive titled "Notice that Funds for Capital Construction Investments Are Supervised and Appropriated by Specialized Banks," appointing the Bank of Communications as the specialized financial institution responsible for managing funds related to capital construction investments.

Subsequently, on June 5, 1951, the central office of the People's Bank of China officially issued the "Instructions on the Bank of Communications Starting to Handle the Central Capital Construction Appropriation Work" from June 1,1951. This document explicitly outlined that the Bank of Communications would oversee the central infrastructure appropriation and also represent investments in agriculture, water conservancy, and forest reclamation.

The Agricultural Cooperative Bank (The headquarters were established in Beijing on 10 July 1951. In July 1952, it merged with the People's Bank of China and its functions were merged into the People's Bank of China.) and the People's Insurance Company of China (PICC, founded in October 1, 1949 and headquartered in Beijing) had 562 branches on the mainland.

Private banks...

In the PLA controlled areas, all private banks are placed under control of the PBC, and they required to deposit 30 % of their reserves in the PBC. Private banks were not allowed to issue loans up to 50% of deposits, to hold stocks in commercial enterprises, and they were prohibited to speculate in commodities.

Until 1952, the state banking system and private banks coexisted, and owners of private banks who had fled to Hong Kong were encouraged to return to Shanghai. For example,

Zhou Zuomin, who went to Hong Kong in 1949 but returned in August 1950 and became the vice president of the national joint state-private bank in December 1952.

Before the Communist takeover of Shanghai, 163 underground CCP members with backgrounds in the banking industry were placed under the direct control of the Central CCP. The CCP focused on the banking sector for two primary reasons. Firstly, banking executives were seen as valuable in preserving bank assets, prompting them to remain in Shanghai. Secondly, middle and higher-ranking employees were considered useful for conducting investigations to prepare for the takeover and reorganization of the banking industry post-liberation.

After the Second Sino-Japanese War, Shanghai capitalists distanced themselves from the Nationalist government, leading to strained relations. As the civil war turned unfavourable for the GMD, the CCP faced increased suppression. In July 1947, CCP members were arrested and executed under martial law, compelling many bankers to leave Shanghai. The financial turmoil and the establishment of the PRC prompted Shanghai capitalists to seek safer business locations, with many choosing to relocate to Hong Kong, instead of Taiwan, where they found a favorable environment for modern entrepreneurial without activities political restrictions.

While Hong Kong served as a safe haven during political turmoil, the outbreak of the Korean War in December 1950 favoured the GMD. Bankers sympathetic to the CCP became hesitant after receiving asset freezing warnings from the U.S. government. Taiwan's alliance with the US positioned the GMD to potentially unfreeze assets in the future, leading Shanghai bankers in Hong Kong to cease aligning with the CCP.

The CCP classified Shanghai banks into 3 types. The first type was owned by bureaucratic capitalists, like the big 4 families. (see Article 1) They were immediately confiscated. Likewise, all "bureaucratic capitalist" owned industries and commercial firms were confiscated and nationalized without compensation.

The second type was the joint state-private bank; these were inherited from the GMD. A new chairman was appointed for each bank and there were put limitations on its private role and the majority of the shares were in the hands of the new administration.

"With respect to the joint state-private banks, the new government inherited all official shares of the old government and verified the legitimate rights of private shareholders. In carefully planning the takeover process, the Financial Division of the Military Control Committee assigned former underground Communist Party members in each bank as special officers in charge of coordinating the transition of old joint banks."

The third type was privately owned small and medium-sized commercial banks and native banks. These private banks were permitted to continue their business after they registered with the new administration. The government set a minimum capital requirement, this way eliminating small banks or forcing them to merge. In Shanghai, all twenty-eight existing native banks, fifteen private banks, and three trust companies consolidated into four joint banking groups. At the end of 1951, only 10 percent of native

banks and other private banks were still independently operating. The PBC received 90% of private deposits and 100% of public deposits. All transactions of governmental institutions, public schools, state owned enterprises are done by the PBC. The PBC had more or less a monopoly on banking and financing.

On December 1, 1952, Shanghai underwent the socialist transformation of its banking and finance sector. All state banks, private banks, and local banks were consolidated into a General Administration of Joint State-Private Banks. This nationalization of banks in Shanghai resulted in a reduction in the number of financial institutions and their staff. Approximately 2,000 former bank employees and 4,500 of their family members were relocated to the remote regions of northwest China to contribute to socialist development in those areas. Other private bankers and staff members were assigned to various financial and economic planning departments within state-owned enterprises and commercial firms.

Foreign banks were allowed to stay after registration, most left the city. The Chartered Bank of India, Australia, and China, The British Mercantile Bank, the Banque de l'Indochine, the Banque Belge pour l'Etranger, the Moscow National Bank, and Hong Kong and Shanghai Banking Company (HSBC) remained in business in part because the UK government established diplomatic relations with the PRC. Before 1939, the HSBC had 14 branches in China; only five branches remained open after 1949; Shanghai, Tianjin, Beijing, Shantou, and Qingdao. Shanghai and Tianjin were in full operation, the other branches were, in fact, out of business and resumed open to settle ongoing business.

In March, 1950, the HSBC management could report to its shareholders that 1949 had been a good year for the bank and would pay the same dividend as previous year.

"There had been no catastrophic change since the inception of the Socialist regime, and the turmoil in mainland China was largely

compensated for by increasing Hong Kong trade and by the transfer of Shanghai’s business in the colony.15"

Fig. 39.5 Trade China with Hong Kong 1949-1954

Source: Source: Shao (1991). Page 66

The US decision to impose an embargo on trade and the decision to freeze all PRC assets in 1951 caused big difficulties for the bank. The bank management decided to close the Shanghai office, however,

"The Chinese authorities reacted with surprise to HSBC’s threat to quit mainland China in 1952, and the Bank of China began to

cooperate actively with HSBC to reduce the cost of maintaining its branches. For example, Chinese authorities permitted, at last,

in December 1954, the closure of the Tianjin office.41"

The Guangdong private banking system, which is an important player in commercial and financial trade with Hong Kong and other capitalist countries, was preserved after the takeover. This policy was called: “three years of recovery, then ten years of development.” In Guangdong, all private banks fell under the oversight of the People’s Bank but were allowed to maintain their autonomy, providing loans to local merchants and accepting deposits from Chinese individuals and businesses. There was a specific focus on local bank assistance for commercial trading with Hong Kong and for managing remittances sent by overseas Chinese to their families in China affected by war. Speculative banking practices, including investments in stocks and land, were prohibited. (See Article 37)

Like all private banks in the PRC, these banks are required to maintain a capital level of 600 million yuan. Other requirements specified the maximum ratio of loans to deposits, a limitation on total loans, a minimum level of liquidity, and the maintenance of required reserves in the PBC.

It should be noted

"Even at best, the Chinese currency only supplemented and never superseded the role of Hong Kong dollars as de facto standard money

in south China"

During Sanfan and Wufan, the employees of private banks were extensively scrutinized. Nevertheless, Chinese government authorities in Guangdong persisted with a pragmatic approach for several years after 1949 to maintain essential trade connections via Hong Kong with the Western world. This crucial linkage facilitated the import of crucial capital goods and the accumulation of financial capital from exports and overseas remittances post-1949.

Agricultural credit...

The expansion of state banking services and the emergence of modern financial institutions such as rural credit cooperatives did contribute to a reduction in rural private lending and addressed capital shortages in rural areas. Private lending after 1949 was subject to some suppression. However, state banks and cooperatives, while formal financial entities, were characterized by strict controls, complex procedures, and a focus on specific loan purposes. In contrast, private lending offered greater flexibility, allowing borrowers to use funds without stringent restrictions, making it a more practical option for immediate production or living needs. Rural private lending played a constructive role in alleviating certain capital shortages and fostering growth in the rural economy. However, a minority of households faced increased poverty due to difficulties in loan repayment, while a small percentage experienced improved status through interest income. Despite the inevitable challenges associated with lending, the positive impacts of private lending should not be overlooked.

However, the notion of free borrowing and lending faced significant obstacles due to the prevailing conditions in rural villages. Middle and wealthy peasants, who could afford to provide small loans to poorer villagers, were simply hesitant to do so. Their apprehensions stemmed from two main concerns. Firstly, they feared that the loans would never be repaid. Government policies and the conduct of local cadres overwhelmingly favored the poor, and the memory of landlords being expropriated without compensation was still vivid, leading most potential lenders to believe that they would never recover their money, let alone receive both principal and interest. Secondly, they were concerned that despite official assurances, their lending activities might be perceived as exploitative by the local community, potentially leading to an elevation in their class status.

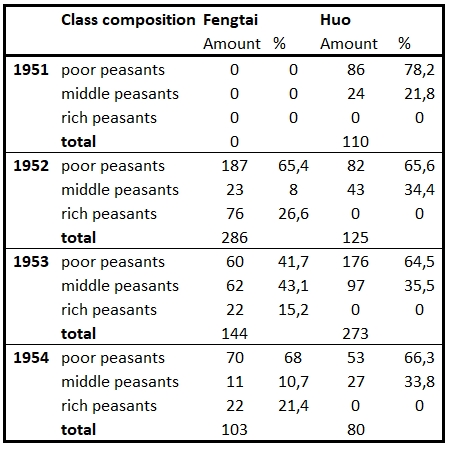

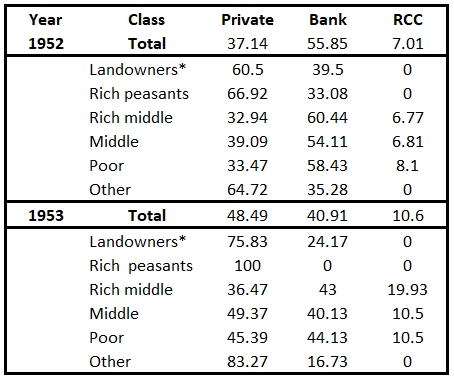

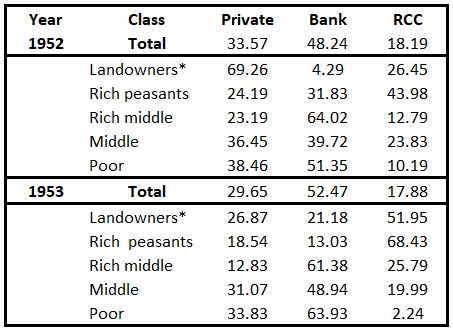

Fig. 39.6-8 Class composition and loan sources in Anhui, Guangdong and Henan

The key factors driving rural private lending post-land reforms included the underdeveloped nature of the rural economy, vulnerabilities in household economies, the absence of a social security system, and the lack of a modern financial infrastructure. The majority of private lending transactions involved poor peasant, hired farmhand, and middle peasant households. While most private loans were used to address immediate living challenges, some were utilized for production purposes.

The earliest rural credit cooperatives in mainland China appeared in the 1920s. Traditional credit institutions for agriculture that had developed during the Republican Era, 1912-1949, institutions including credit cooperatives and formal banks such as the Farmers’ Bank of China (1935) developed under the Rural Reconstruction (1928- 1937) and the Farm Credit Bureau (1936) were annulled. Before 1949, the CCP initiated a restructuring of the rural financial system by introducing rural credit cooperatives (RCCs) in regions under CCP control. These cooperative entities, initially owned by their members, offered savings and loan services to small agricultural producers. Beyond their financial role, the establishment of RCCs had political and ideological motives. They were created to shield peasants from exploitative money-lending practices prevalent under the GMD government. Consequently, they can be viewed as an early social policy intervention, aimed at enhancing rural welfare and fostering greater equality, rather than merely serving as financial intermediaries. Two types of RCC existed:

1. Credit Mutual Aid Teams; small scale cooperatives which deal within the mutual aid teams.

2. Credit Union of Supply and Marketing Cooperatives. Its funds are furnished by the members and the PBC supervises and aids in financial management

Shortly after assuming power, the CCP continued the restructuring of the rural financial system. In addition to RCCs, the Agricultural Cooperative Bank was founded to provide 'policy loans' aimed at financing agricultural production. The RCC network expanded across the nation, solidifying its position as the primary financial service provider for rural households engaged in farming activities.

In May 1951, the first national rural financial work conference decided to establish various rural credit cooperative organizations on a trial basis across the country. After the CCP passed the "Resolution on the Development of Agricultural Producer Cooperatives" in December 1953, rural credit cooperatives developed rapidly. By the end of 1952, there were 20,067 pilot credit cooperative organizations across the country; by the end of 1953, the number had grown to 25,290.

Fig. 39.9 Agricultural Loan from 1950 to 1952

Wang (2019). Page 31 The unit of loans is 100 Million Yuan.

In 1950, during the rural land reform period, national banks initiated the issuance of in-kind loans. According to Gansu rural financial gazetteers, the total grain distributed exceeded 360,000 shidan (75 kg each) in 1950, and this figure expanded to over 434,000 shidan in the first half of 1951. At the onset of 1950, the Central South Branch of the People’s Bank of China allocated 2.1 million kilograms of rice, including 1.53 million kilograms of rice in kind, as agricultural loans to Guangxi province. The aim was to facilitate the resumption of agricultural production and support rural activities in Guangxi. In-kind agricultural loans primarily consisted of rice and required repayment in the same form. These loans were extended to impoverished farmers, with the primary purpose of funding the construction of small water-conservancy projects, acquiring farm tools, and purchasing seeds and fertilizers. Loans were categorized into three groups:

1. Production Loans: Initially, there were long-term loans (spanning one to three years) designated for the acquisition of significant agricultural equipment and technical enhancements. These loans were primarily directed towards Mutual Aid Teams, Agricultural Production Co-ops, and state-managed collective farms. Additionally, there were shorter-term, smaller loans for fertilizer, seed, and tools provided to financially challenged peasants facing production difficulties. While Mutual Aid Teams were given preference, some independent peasants also qualified for these smaller loans.

2. Loans for Transportation and Marketing of Agricultural Products: Typically directed towards state trading companies or local Supply and Marketing Co-ops, these loans aimed to assist in the procurement and distribution of agricultural and sideline products. Loans under this category were also extended to private merchants and companies to boost trade, with the objective of complementing rather than disrupting state-run commerce.

3. General Purpose Capital Loans: This category encompassed loans for various purposes, including clothing, medicine, house repairs, funerals, weddings, and small sums allocated to enable peasants to participate in sideline occupations.

Foreign currency and Stock exchange...

On February 10, 1950, the GAC decided that all foreign exchange holdings, including those of overseas Chinese, foreign travelers, and foreign embassies and missions, be deposited

with the Bank of China, the only bank authorized to deal in foreign exchange. The renminbi was virtually inconvertible. The official exchange rate in 1952 - 1954 was the Yuan per US dollar: 2.617.

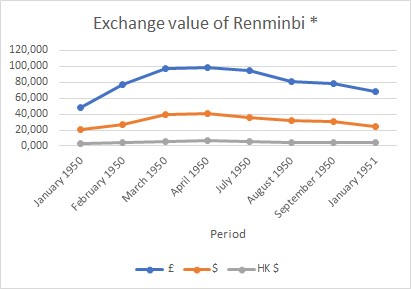

Fig. 39.10 Exchange value rmb against $, £ and HK$

Source: Burdekin (2008). Page 13

The renminbi depreciated by 100% against the US dollar, by 106% against the pound sterling, and by 115% against the Hong Kong dollar between January and March 1950.

In Guangdong, large amounts of European and American currencies circulated in the local economy. The PBC became the only legal institution in Guangdong that holds foreign currency deposits. The PBC emerged as the sole legal entity in Guangdong authorized to hold foreign currency deposits. This move compelled local Chinese banks to cease currency trading and speculation, which had been a significant revenue stream, and required private foreign currency deposits in local banks to be transferred to the BOC. While a select few local banks retained authorization from the BOC to serve as foreign currency dealers, their activities were tightly regulated and confined within the purview of BOC oversight, limiting their ability to trade foreign currencies independently.

Private citizens were permitted to hold only two ounces of gold and four ounces of silver, they were not allowed to transfer or trade these metals without special authorization. The remainder of precious metals had to be exchanged at the PBC for renminbi.

Shao (1991) notes

"It was not until July 1950 that the Bank of China was able to establish a single unified foreign exchange rate for the whole nation;

the next year Shanghai's foreign exchange was abolished, and foreign currencies as well as gold were removed from the sphere of free

transaction. " In 1949, the PRC allowed 2 Stock Exchanges to exist. Tianjin Stock Exchange was officially opened on June 1, 1949 and abolished on July 21, 1952. On January 30, 1950, the reformed Beijing Stock Exchange is reopened and closed October 1952. The Tianjin Stock Exchange traded 10 stocks; the Beijing Stock Exchange traded 6 stocks. They included companies like; Qixin Cement, Kailuan Coal Mine, Dongya Wool Spinning, Renli Wool Spinning, and Yaohua Glass. The Shanghai Stock Exchange was closed in 1949.

Notes...

Fiat money is a type of money that is not backed by any commodity such as gold or silver, and typically declared by a decree from the government to be legal. [↩]

Hsia (1953) The CCP undertook the task of currency unification in two phases. One phase was the redemption of currency issued by the GMD government. The other phase was the consolidation of various currencies issued by the CCP. (There were at least ten different types of currency circulating in the areas of mainland China) For example, the silver notes issued by the Provincial Bank of Xinjiang are replaced by the Renminbi in October 1951. Page 73 [↩][Cite]

Szuprowicz (1978). "As the People’s Bank of China’s subsidiary and a special agency of the State Council, the Bank of China (established in 1912), as late as 1978 it still had some of its original shareholders and was only 66 per cent owned by the PRC government." (Those shares belonging to "war criminals" were confiscated. Since 1956 all private shareholders have only received "fixed dividends" at a rate of five per cent on the basis of their original investment. Pages 75–8.[Cite] See RMRB 23-03-1950 "The Government Affairs Council of the Central People's Government issued an order to strengthen the supervision of the leaders of the Bank of China and designated Nan Hanchen and others as state-owned directors and supervisors."

By the end of October 1951 there were 5300 branches of the PBC and less than 200 private banks.[↩]

Ji (2003). Pages 361-362. [Cite] In a Memorandum (December 2, 1949) by the Chief of the Division of Security (Nicholson) to Mr. Robert W. Barnett of the Office of Chinese Affairs it is noted that 2 ships arrived at San Francisco with 2 million dollars in United States currency. This money originated with the People’s Bank of China, but the transfer was handled through the Banque Belge Pour L’Etranger and the Banque De L’Indochine. See document 02-12-1949 Memorandum by the Chief of the Division of Security [↩]

Burdekin (2008). Pages 57-58. Two series of bonds in 1950 and 1954–1958 are issued.[Cite] See documents 04-12-1949 Decision of the CPGC on Issuing People's Victory Discounted Public Bonds 09-12-1953 Regulations on National Economic Construction Bonds in 1954 Hayashi (2022) gives an example of Chongqing: Purchasing bonds were allocated to each enterprise.The allocation was proportionate to the size of each enterprise. The highest allocation was for the shipping industry at 220,300 units, followed by the cotton textile industry (207,287 units), the mountain product industry (188,900 units), the banking industry (187,348 units), and the salt trading industry (144,051 units). Together, these five industries accounted for 45 percent of the total amount of 2,107,448 units. Page 55

[↩][Cite]

Gao (2004). Page 81 "From July to November 1949, the price indices increased by 180 percent Beijing and Tianjin, by 150 percent in Shanghai and other cities in Central and Northwestern China. The general inflation continued in the early 1950. Using December 1949 as the base month,the price indices advanced from 100 to 226.3 in March 1950 and did not decline until April." Note 88 [↩][Cite]

Li (2021). "Only one month after liberating Sichuan, Deng supported Chen Yun in collecting 400 million jin of grain from Southwest China for transport to Shanghai in order to control unstable prices in East China.9" Page 3 [↩][Cite]

From 1951 to 1954, capital construction expenditures in the national financial budgets at all levels totalled 25.6 billion yuan, accounting for about 1/3 of the total state financial budget expenditures of 76.5 billion yuan in the same period, of which nearly 20 billion yuan was allocated through the Bank of Communications. [↩]

Niu (1994). "Between 1911 and 1949, the insurance industry in China was dominated by British companies 1 and the

role of Chinese and other nationals was limited" Page 216 [Cite] Hsiao (1967). " In 1949, the regime set up a Chinese People's Insurance Company to cover all policies.51 Like the Chinese People's Bank which has a Bank of China as its foreign exchange agency, the Chinese People's Insurance Company is also assisted in its foreign operation by two state-private joint establishments: the China Insurance Company, Limited, and the Tai Ping Insurance Company, Limited. Together they maintain an extensive network throughout the world, except North America,..." Page 312 [↩][Cite]

Peruzzi (2017). Page 21

"统一财经后,中国人民银行统一管理外汇牌价与外汇调度,授权中国银行管理外汇与经营外汇,并选择一些在国外有分支行或代理行,有一定的外汇资金,向来信誉较好、遵纪守法的外资银行、私营银行,经严格审查后核准为指定银行,代理中国银行经营外汇。之所以准许除中国银行外的“指定银行”经营外汇业务,主要是考虑到一些外资银行、私营银行已有一定国际金融资源储备,不论是人力、物力还是与国外市场的关系,都能在对外贸易、国际金融中发挥桥梁作用,作为国家银行领导下外汇业务的重要补充。指定银行的外汇业务主要是:(1)进出口押汇及代收外汇;(2)进出口的外汇贷款;(3)国外汇兑;(4)买卖外汇。指定银行主要分布在北京、天津、上海、青岛、南京、杭州、泉州、厦门、汉口、长沙、广州、汕头、重庆、昆明等14个城市,私营银行主要是:上海银行、新华银行、金城银行、国华银行、中国实业银行、浙江兴业银行、中南银行、聚兴诚银行、建业银行、浙江第一银行、和成银行等11家银行;侨资银行有:东亚银行、华侨银行、集友银行等3家银行;外商银行主要有:汇丰银行、东方汇理银行、加利银行、华比银行、有利银行、荷兰银行等6家银行。到1952年,指定银行只留下汇丰银行、渣打银行(麦加利银行)两家英商银行,以及东亚银行、华侨银行、集友银行三家侨资银行" 新中国金融史 | 国民经济恢复时期金融工作概览. 中国金融思想政治工作研究会新中国金融史编写组

2023-05-08 https://app.dahecube.com/nweb/news/20230508/161800n3d7a6796f22.htm?artid=161800

Translation "After the unification of financial policies, the People's Bank of China centralized the management of foreign exchange rates and foreign exchange allocation. It authorized the Bank of China to oversee and operate foreign exchange activities. Additionally, certain foreign-funded banks and private banks with overseas branches or correspondent banks, adequate foreign exchange reserves, a strong reputation, and compliance with laws and regulations were approved as designated banks to act on behalf of the Bank of China in conducting foreign exchange operations. These approvals followed a rigorous review process.

The primary reason for allowing designated banks, in addition to the Bank of China, to handle foreign exchange business was to leverage their existing international financial resources. These banks had established human and material resources as well as connections with foreign markets, enabling them to serve as vital intermediaries in foreign trade and international finance under the leadership of the national bank. This supplemented the state’s foreign exchange operations.

The foreign exchange operations of the designated banks mainly included: Import and export financing and foreign exchange collection; Foreign exchange loans for import and export; International remittance; Foreign exchange trading.

The designated banks were primarily distributed across 14 cities: Beijing, Tianjin, Shanghai, Qingdao, Nanjing, Hangzhou, Quanzhou, Xiamen, Hankou, Changsha, Guangzhou, Shantou, Chongqing, and Kunming.

The private banks included 11 institutions, such as: Shanghai Bank, Xinhua Bank, Jincheng Bank, Guohua Bank, China Industrial Bank, Zhejiang Industrial Bank, Zhongnan Bank, Juxingcheng Bank, Jianye Bank, Zhejiang First Bank, Hecheng Bank

The overseas Chinese-funded banks included 3 institutions: East Asia Bank, Overseas Chinese Bank, Jiyou Bank

The foreign-funded banks primarily included 6 institutions: HSBC, Crédit Agricole, Cali Bank, Banque Belge pour l'Étranger (Belgian Bank), Mercantile Bank of India, Netherlands Trading Society

By 1952, the designated banks had been reduced to just five: two British-funded banks (HSBC and Standard Chartered Bank, formerly known as Mercantile Bank of India) and three overseas Chinese-funded banks (East Asia Bank, Overseas Chinese Bank, and Jiyou Bank)."

Source: History of New China's Financial System | Overview of Financial Work During the National Economic Recovery Period. Compiled by the Editorial Group of the Financial Ideological and Political Research Association of China. Published on May 8, 2023.

[↩][Cite]

Su (2016) notices "...middle peasant households were unwilling to lend even if they had excess grain, for fear of “exposing wealth,” or “standing out,” or “elevating status,” or being labeled “usurers.” " Page 239 [↩][Cite]

Wang (2019). "...loans were used for self-consumption accounted for the largest proportion. For instance, it was 68% for consumption, 15% for in-kind agricultural tax, 8% for seed fertilizers purchase, and 9% for business and others in 1950. While in 1951, it was 57% for consumption, 10% for grain consumption and seed fertilizer purchase, and 33% for business and others4" Page 41 [↩][Cite]

Su (2016). Pages 231-266 "Surveys conducted after 1949 indicated that in the period between land reforms and the imposition of the state grain monopoly, most rural private loans were in grain, that even those made in cash were denominated in terms of grain, and that forms of loans were simpler than they

had been prior to 1949. Once the state monopoly had been instituted, most loans were made in the form of cash." Page 248 [Cite] Wang (2019) "At the first National Finance Conference 1 after the PRC was founded, it was pointed out that informal lending should be encouraged in both old and new liberated rural areas. In December 1950, at the Second National Finance Conference, it was pointed out that informal lending was

better than nonexistence of lending channels 2, although the interest rate was higher in informal market....In July 1953, the State Council affirmed the rightful status of rural informal lending by releasing report “Instructions on Issuing Agricultural Loans”. The State Council pointed out that “At present, national banks cannot fully meet the credit needs of farmers and RCCs were not generally developed, rural informal lending is still needed by farmers and should be allowed to exist and develop 44." Page 40 [↩][Cite]

Zhang (2013). Pages 7-8 Chongqing Rural Credit Cooperative founded in 1951, Jiangyin Rural Commercial Bank established in 1953[↩][Cite]

01-03-1950 Provisional regulations on currency control Regulations for the Central Treasury. March, 3, 1950.

Decree of the GAC on strengthening the guidance and supervision of the Bank of China. March 22, 1950.

Decision of the GAC regarding the enforcement of cash control in state organs. April 7, 1950.

Standard Rules for the Articles of the Rural Credit Cooperatives (Draft). December, 1950

Convention on Rural Credit Mutual-help Group (Draft). December, 1950

25-12-1950 Regulation on the implementation of currency control Directive of the Finance and Economics Committee regarding the “Measures for enforcement of monetary control”. December 25, 1950.

Measures for the preparation of the monetary receipt and disbursal plan. December 25, 1950.

Provisions of the Finance and Economics Committee of the GAC regarding applications from United States enterprises and individuals for withdrawal of their deposits. January 14, 1951.

The People's Bank of China issued the "Notice that Funds for Capital Construction Investments Are Supervised and Appropriated by Specialized Banks" February 1, 1951

Measures prohibiting the movement of the nation’s currency into and out of the national territory. March 6, 1951.

Decree of the GAC recalling currencies issued for local circulation by the Northeast Bank and the People’s Bank of Inner Mongolia. March 20, 1951.

19-04-1951 Interim regulations on punishment for impairment of state currency Decree of the GAC regarding the people’s money bearing notations in the Uighur language, issued in Sinkiang, and permission for its nationwide circulation. September 21, 1951

15-10-1952 Interim measures for prohibition against bringing negotiable instruments and securities in the state currency into and out of China Measures of the GAC for the payment of nonreimbursed deposits made in banking houses before the liberation. February 20, 1953.

Measures for the registration of nonreimbursed deposits made in banking houses before the liberation. 1953.

Directive of the GAC regarding the establishment of the People’s Construction Bank of China. September 13, 1954.